Submitted by Charles Hugh-Smith of OfTwoMinds blog,

Gasoline is expensive at the pump, but by one measure oil is cheap and poised to go higher.

I recently posed this question to longtime contributor Harun I.: could global hot money flow into the crude oil market, driving the price up even if demand declines? The basic idea here is that if equities, bond and housing markets soften or roll over (please see What If Stocks, Bonds and Housing All Go Down Together? May 24, 2013), global hot money will seek speculative gains elsewhere.

In an era of rising geopolitical tensions (see Syria), what better place to notch a speculative gain than oil and gold?

Put another way: Is oil cheap? Harun offered a chart of the crude oil/gold ratio (in effect, crude oil priced in gold rather than nominal U.S. dollars) and the following insightful commentary:

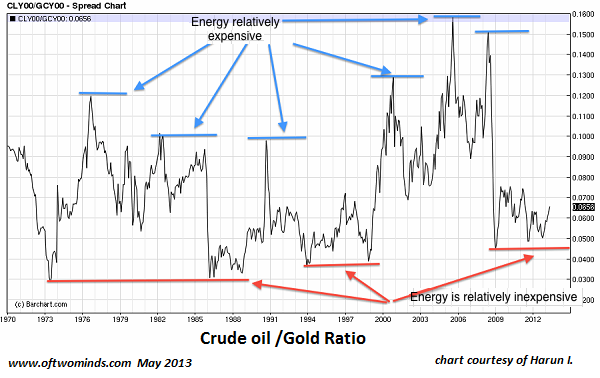

Very good question. I suggest we not make the error of just considering nominal price. For example, below is a chart I marked up about a week ago, the Crude Oil/Gold ratio. I like relative-strength charts because they are a better indication of high and low prices and they tend to oscillate within a range. Here we see a history going back to the 1970s.

At the highs and lows consider what this meant to the economy at that time. What I find rather interesting is that, currently the chart is indicating crude oil is relatively inexpensive. However, one trip to the pump says something entirely different. In fact, prices at the pump are not far off their peak from when this ratio was at its height.

Now imagine what would happen to prices if this ratio returns to its high. Remember this is relative, there could be a demand collapse and this ratio could still go to its historic high. What would that look like in the economy? Well much like the Great Depression, plenty of stuff but no money to buy it. Commodities are real and the effects of hot money are felt almost immediately causing demand to collapse quickly because the real people that make up the economy don't eat paper. If hot money flows into crude oil driving pump prices to $8.00/gallon it would devastate the economy even further.

The Fed is trapped. There were no good answers in 2000, 2008, or now. But the room has gotten a lot smaller.

The reflationary bubble in equities has acted as a hedge but it has not increased purchasing power. No wealth has been created for the middle class. This is why the Fed cannot lift off the accelerator. Therein lies the problem. How does the Fed square the divergence of the equity markets and its monetary stance? How can it continue to claim that they are not the cause of inflation or bubbles?

Where will money flow? It may foment mini-bubbles in all things tangible, classic cars, precious metals, art, etc., as the wealthy scramble to get out of cash. But there will be no place to hide. This will get messy, but the revealing of really big lies always is.

The chart above is cause for grave concern. The fact that it is indicating that energy prices are cheap and have no place to go but up is sounding an alarm. It is my opinion that the average person is in no place (in terms of purchasing power) to absorb a return to the relative highs on this chart.

Thank you, Harun, for the chart and the commentary. You see what happens when oil becomes expensive: the economy sinks into recession.

The conventional wisdom is that oil should decline in nominal price as global demand weakens along with the global economy.

In the hot-money-seeks-a-new-home scenario outlined above, demand could decline on the margins but speculative inflows--demand for oil contracts by speculators--push prices higher, potentially a lot higher in a geopolitical crisis.

The central banks that are creating all the "free money" that is available to large speculators fulminate against oil speculators, as if all the free money is only supposed to go to "approved" speculations in equities and bonds.

Unfortunately for the central bankers, they only create the money, they don't control what the financiers who get the free money do with it.

Despite the endless MSM hype about U.S. energy independence and U.S. exporting energy abroad, the U.S. still imports over 3 billion barrels of crude oil every year:U.S. Imports of Crude Oil (U.S. Energy Information Administration).

Demand for imported crude oil fell 4.9% from 2011 to 2012, tracking lower gasoline consumption and miles driven. But that's still a figurative drop in the bucket of oil imports. Anyone who believes the U.S. is impervious to geopolitical oil shocks is on a Fantasyland ride with an abrupt stop in terribly inconvenient reality.